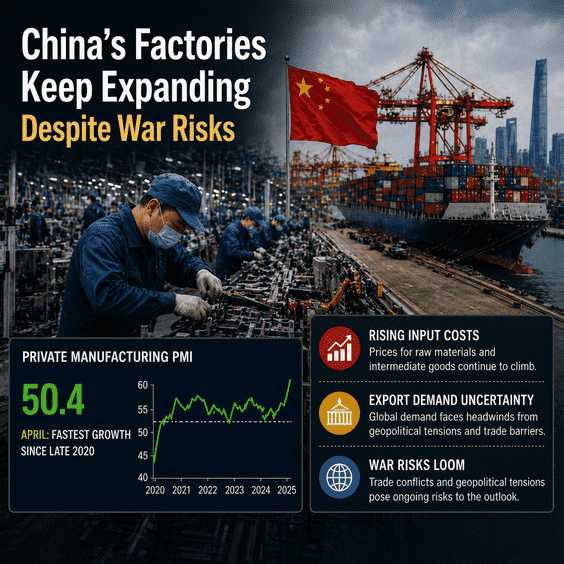

A private PMI shows manufacturing growth at its fastest pace since late 2020, but rising input prices and uncertain export demand cloud the rebound.

BEIJING, MAY 1, 2026

China’s factories entered the second quarter with a burst of momentum that would normally calm fears about the world’s second-largest economy. The private RatingDog China General Manufacturing PMI, compiled by S&P Global, jumped to 52.2 in April from 50.8 in March, beating forecasts and marking the fastest expansion since late 2020. Output strengthened, new orders surged and export business expanded for a fourth consecutive month. On the surface, the data describe a manufacturing sector rediscovering speed.

A PMI above 50 signals expansion, but the composition of the increase matters. In April, the acceleration was concentrated in output, new orders and purchasing activity, the parts of the survey most closely tied to immediate production schedules. That points to factories running harder now. It does not automatically mean households are spending more, companies are hiring aggressively or exporters have visibility deep into the year. The PMI is an early signal, not a guarantee of a cycle.

Underneath, the picture is more complicated. The same survey that captured the strongest headline reading in more than five years also showed a sharp build-up in cost pressure. Energy and raw-material prices pushed input inflation to its highest level in just over four years, while factories raised output and export prices at the fastest pace since October 2021. That is not a footnote. It is the key tension in China’s latest recovery signal: production is rising, but so is the cost of producing, shipping and pricing goods in a world unsettled by war risk.

The cost data are especially important because China has spent years fighting producer-price weakness. A mild return of factory-gate pricing power can help companies repair balance sheets, but a war-driven input shock is different. When oil, chemicals, metals and freight costs rise together, price increases can feel less like healthy demand and more like imported stress. Firms with global brands or specialised products may pass that stress on. Smaller suppliers in crowded sectors may not.

The official survey’s sector detail points to the same squeeze. Raw-material price gauges remained elevated, while output-price measures suggested limited pricing power. Petroleum, coal-processing and chemical-related sectors saw especially high price pressure. That matters for China’s vast downstream supply chain, from plastics and packaging to auto parts and consumer appliances. A cost shock in those upstream industries does not stay there; it moves through the factory ecosystem with a lag.

The immediate backdrop is the Middle East conflict and the uncertainty it has injected into energy markets, shipping routes and purchasing decisions. Chinese manufacturers have benefited from buyers trying to secure goods early before costs rise further. In that sense, war risk is creating short-term demand. Overseas customers that fear price spikes, delayed deliveries or supply disruptions have pulled orders forward, giving exporters a stronger April than many analysts expected. The official PMI also stayed in expansion at 50.3, with export orders rising to their strongest level in two years.

But front-loaded demand is not the same as durable demand. Once customers have stocked warehouses and absorbed higher prices, the next phase can be weaker. That is why the sustainability of April’s factory strength is now the central question. If energy costs remain elevated, importers in Europe, Asia and the United States may order less later in the year. If freight and insurance costs rise, margins will be squeezed again. If global consumers slow under the weight of inflation, China’s export machine could lose momentum just as domestic demand remains uneven.

The divergence between the private and official surveys reinforces that point. The official manufacturing PMI, which leans more heavily toward larger and state-linked firms, dipped slightly from March while staying above the 50 mark that separates expansion from contraction. The private RatingDog survey is more sensitive to private and export-oriented producers, especially those clustered around China’s coastal and southern manufacturing regions. Its stronger reading suggests that external demand is doing much of the heavy lifting. That is good news for factories with foreign customers, but less reassuring for policymakers who want a broader, more consumption-driven recovery.

The weakness outside manufacturing is visible. The official non-manufacturing PMI, covering services and construction, fell to 49.4 in April, back below the growth threshold. China’s property slump continues to weigh on construction, household confidence and local government finances. Retail sales have trailed industrial output, and unemployment has edged higher. The economy grew 5% in the first quarter, at the top of Beijing’s full-year target range of 4.5% to 5%, but that resilience has rested heavily on production, exports and policy support rather than a decisive rebound in household spending.

For Beijing, April’s PMI data create both comfort and risk. The comfort is that manufacturing remains capable of absorbing shocks. China’s industrial base can scale quickly, reroute orders and use its deep supplier networks to respond when global buyers become nervous. The country’s energy reserves and diversified supply channels also give it buffers that many rivals lack. The risk is that the economy becomes even more dependent on a factory-led model just as external conditions deteriorate. A growth engine powered by exports is vulnerable when the outside world is preoccupied with war, oil prices and protectionist politics.

There is also a global inflation angle. For much of the past few years, Chinese goods disinflation helped soften price pressures abroad. If Chinese manufacturers are now passing higher input costs into export prices, that channel weakens. The April survey showed some firms were able to transfer costs to buyers, though others continued to absorb them in thinner margins. Either outcome carries consequences. Passed-through costs can add to goods inflation in importing countries. Absorbed costs can weaken Chinese corporate profits, discouraging hiring and investment even while output rises.

Employment is already the soft spot in the private survey. Despite stronger output and backlogs, firms remained cautious about adding workers. That caution matters because China needs factory strength to translate into income, confidence and domestic demand. Without hiring, a production rebound can look impressive in PMI tables while doing less to repair household sentiment. Backlogs rose for a third month, suggesting capacity pressure, but companies appear reluctant to treat the current order book as proof of a lasting upswing.

Policy expectations are therefore shifting. With first-quarter growth solid and manufacturing in expansion, analysts see less urgency for high-profile monetary easing. Beijing’s leadership has instead emphasised energy security, technological self-sufficiency and the need to withstand external shocks. Those priorities fit the moment. The war-risk environment rewards countries that can secure inputs, move up the value chain and reduce exposure to volatile foreign supplies. Yet those same priorities do not answer the weaker-consumption problem at home.

The next confirmation will come from trade, profit and employment data rather than PMIs alone. If exports accelerate in May and June without a collapse in margins, April’s survey will look like the start of a stronger external cycle. If orders fade after stockpiling and companies remain reluctant to hire, the PMI will look more like a temporary war-risk surge. For now, the factories are busy, but the business model is carrying more geopolitical risk on every invoice.

April’s manufacturing data are, then, a strong number with a warning label. China’s factories are expanding faster than at any time since the post-pandemic rebound, and export orders show that global buyers still rely on Chinese production when uncertainty rises. But the rebound is being fed partly by stockpiling, price effects and external anxiety. The more war risk drives demand today, the more fragile that demand may look tomorrow. For China, the question is no longer whether factories can accelerate. It is whether they can keep accelerating after the rush to get ahead of higher costs has passed.