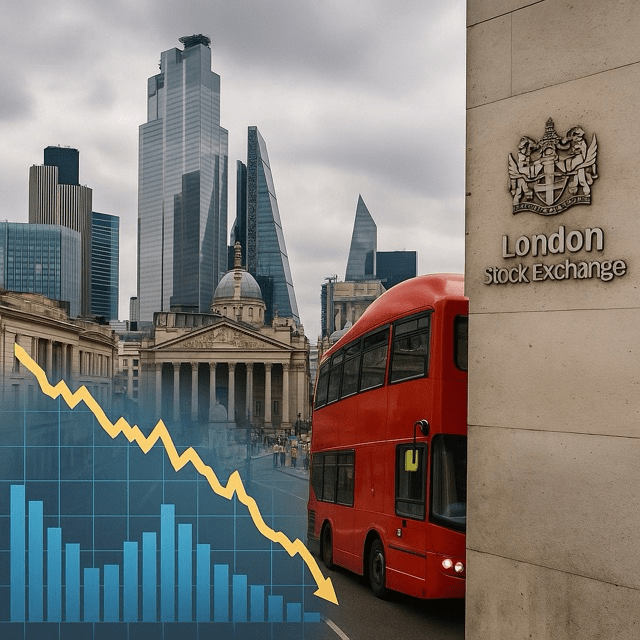

What’s Behind the Surge of Delistings and What It Means for London’s IPO Market

Since the buoyant initial public offering (IPO) wave of 2021, when high-profile companies flocked to London markets seeking capital and prestige, nearly 25% of the largest listed firms have quietly exited. According to data from the London Stock Exchange (LSE), out of the 40 biggest IPOs in that year—ranging from fintech disruptors to green-energy pioneers—ten have delisted, been acquired, or transferred their primary listings abroad, leaving investors and regulators searching for answers.

The trend accelerated in late 2023, as global economic headwinds and sector-specific setbacks prompted companies to rethink public-market strategies. Among the notable departures were two fintech unicorns that cited valuation mismatches and mounting compliance costs as key factors in their decisions to delist and restructure as private entities. Similarly, a major renewable-energy developer was snapped up by a strategic investor, motivated by a generous takeover bid that analysts estimate was 30% above its peak market capitalization on the LSE.

Industry experts argue that several forces converge to drive this wave of exits. First, market volatility since the onset of the COVID-19 pandemic has depressed share prices, making public-market financing less attractive. Second, the regulatory burden—especially under the UK’s Senior Managers and Certification Regime and EU’s Sustainable Finance Disclosure Regulation—has increased operating costs for smaller public firms. Third, alternative funding channels such as venture capital, private equity, and special purpose acquisition companies (SPACs) have matured, offering more flexible terms outside public scrutiny.

Investors have voiced mixed reactions. While early backers of these companies may have reaped significant gains during IPO pops, longer-term shareholders faced elongated periods of illiquidity, especially when trading volumes thinned amid broader market sell-offs. “The flash IPO rally masked deeper challenges,” says Maria Thompson, portfolio manager at Wellington Asset Management. “For many of these firms, the market simply did not provide the support or stability needed for sustainable growth.”

From a regulatory standpoint, the LSE and the Financial Conduct Authority (FCA) are under pressure to bolster market appeal and credibility. Proposals under discussion include streamlining compliance requirements for mid-cap firms, enhancing post-IPO investor engagement, and expanding the UK’s Growth Market regime to attract smaller listings without hefty disclosure obligations.

Despite the departures, London remains a global financial hub. In the first half of 2025, the UK capital saw a modest resurgence of listings, led by biotech firms and sustainable infrastructure companies, which are perceived as better equipped to meet stringent ESG (environmental, social, governance) standards. Notably, three foreign domiciled firms completed secondary listings in London this year, signaling continued confidence in the city’s depth of capital and investor base.

Yet the 2021 cohort’s attrition serves as a cautionary tale. “IPOs are not an endpoint but a milestone,” notes Sophie Lee, head of corporate advisory at KPMG UK. “Companies must align their capital structures and governance frameworks to the realities of public markets, or face the prospect of underperformance and eventual exit.”

Looking ahead, the key question is whether London can recalibrate its offering to retain dynamic growth companies. That may involve embracing dual-class shares or tailored index benchmarks, which the US and Asia-Pacific exchanges have used to lure tech giants. It may also require reinforcing the UK’s reputation as a transparent, resilient market amid geopolitical and economic uncertainties.

For investors, the message is clear: diligence is paramount. Scrutiny of corporate governance, cash-flow forecasts, and regulatory roadmaps should accompany any IPO investment decision. As London’s 2021 listing stars fade from public view, the next wave of market entrants will need to demonstrate not just innovation, but the fortitude to navigate the complexities of the public domain.